What Actually Replaces Your Paycheck In Retirement

Most people spend 30 or 40 years working toward a number.

A balance. A nest egg. A “retirement goal.”

But almost no one stops to ask the more important question:

What actually replaces my paycheck when my job stops?

Because in retirement, the problem isn’t how much money you have.

It’s how much money shows up — month after month — whether the market cooperates or not.

The Quiet Shift No One Prepares You For

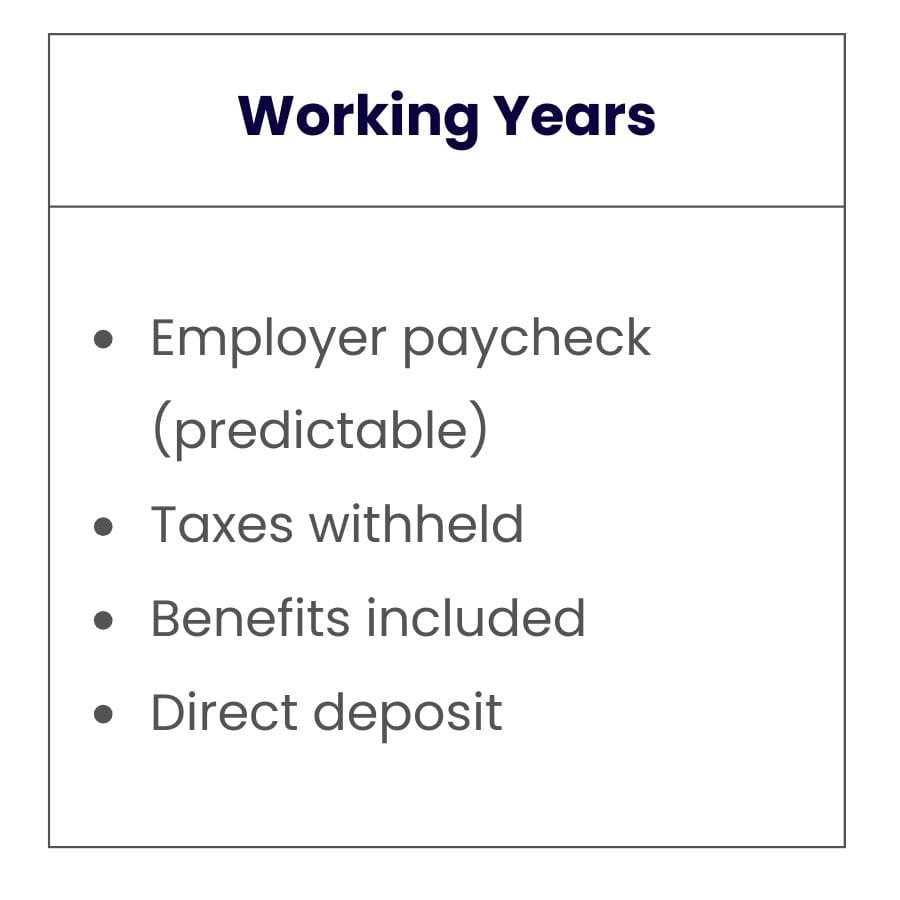

When you’re working, life runs on a simple system:

Work → Get Paid → Pay Bills → Live Life

In retirement, that system disappears.

Suddenly, you become the one responsible for creating your own paycheck. And for many people, that’s when the anxiety starts — not during a market crash, but on a calm Tuesday morning when they realize:

“I don’t actually know where my monthly income is supposed to come from.”

This is the moment most retirement plans quietly fail.

Not because the investments went to zero — but because there was never a clear income system in the first place.

The Difference Between a Portfolio and a Paycheck

A portfolio answers this question:

“How much is my money worth today?”

A paycheck answers a different one:

“How much can I safely spend this month — and next year — and ten years from now?”

Those are not the same problem.

Growth is about potential.

Income is about reliability.

One looks good on a statement.

The other lets you sleep at night.

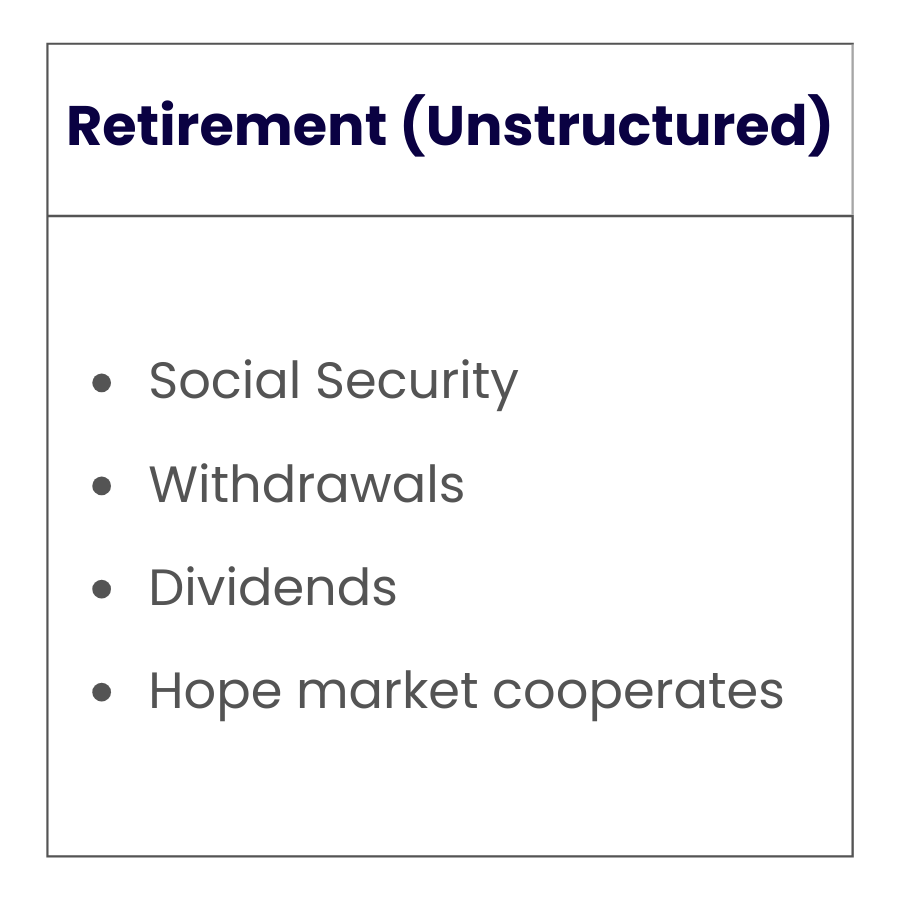

The Three Types of Retirement Income (Most People Only Use One)

Think of your retirement like a three-legged stool. If one leg is weak, the whole thing wobbles.

1. Guaranteed Income

This is money that shows up whether markets are up, down, or sideways.

Examples:

Social Security

Pensions

Contracted lifetime income sources

This is your foundation. It covers your non-negotiables: housing, utilities, food, healthcare.

2. Flexible Income

This is money you can pull from accounts you control.

Examples:

IRAs

401(k)s

Brokerage accounts

This gives you freedom — travel, hobbies, helping family, handling surprises.

3. Growth Income

This is money designed to keep pace with inflation over time.

Examples:

Market-based investments

Long-term growth strategies

This is your future-proofing.

Most people retire with only one leg — flexible income — and hope the market behaves.

Hope is not a strategy.

The Question That Changes the Entire Conversation

Instead of asking:

“How much do I have saved?”

Try asking:

“Which of my bills must be paid no matter what the market does?”

Write them down:

Housing

Utilities

Insurance

Food

Medical

Now ask:

“What income shows up every month to cover these — without me having to sell something?”

If the answer is “Mostly Social Security,” you’ve just identified the real gap in your plan.

Why This Feels Uncomfortable (And Why That’s Normal)

Most people are taught how to save.

Almost no one is taught how to turn savings into income without breaking the system.

That’s why conversations about retirement income feel heavy. You’re not just making a financial decision — you’re making a lifestyle decision that may last 20 or 30 years.

This isn’t about chasing returns.

It’s about protecting your ability to live the way you’ve worked for.

A Simple Exercise That Brings Clarity

Take five minutes and do this:

Step 1: List Your Monthly Non-Negotiables

These are expenses that don’t go away if the market has a bad year.

Step 2: List Your Guaranteed Income Sources

Social Security. Pension. Any income you don’t have to manage.

Step 3: Find the Gap

Subtract guaranteed income from non-negotiable expenses.

That number — positive or negative — is your Retirement Paycheck Gap.

This is the number every smart income strategy is built around.

Where Most People Go Wrong

They try to solve an income problem with an investment solution.

Those tools can work — but only when they’re part of a system, not the entire system.

The goal isn’t to grow money forever.

The goal is to make sure your life is funded for as long as you’re here to live it.

A Calm Next Step (No Pressure)

If you’d like, I’ve put this into a simple one-page worksheet called:

The Retirement Paycheck Map

It walks you through:

Your guaranteed income

Your essential expenses

Your personal income gap

Most people tell me it’s the first time their retirement actually felt organized instead of overwhelming.

You can download it here: [https://www.retirementpaycheckmap.com/ ]

And if after you fill it out you want a second set of eyes on it, I’m always open to a conversation. Not to sell you anything — but to help you make sense of what the numbers are really saying.

Final Thought

Retirement isn’t about reaching a number.

It’s about creating a paycheck that doesn’t depend on your alarm clock.

Once you solve that, everything else becomes a lot less scary.